FCA Car Finance Redress Scheme: What It Means, Who Can Claim, and What Happens Next

Posted on 30 March 2026 by Cory Waterworth

The FCA has confirmed it will set out its approach to motor finance redress shortly after markets close on Monday 30 March 2026.1 This follows months of consultation and years of legal proceedings – and it marks a decisive moment for the millions of people who took out car finance between 2007 and 2024 without being properly told about the commissions built into their agreements.

At Allegiant, we have been advising clients on car finance commission claims since this area first gained regulatory traction, and we have followed every twist in the legal and regulatory story closely. In this article we explain what the FCA’s redress scheme is, who it covers, what you might be entitled to, and what you should do now.

What is the FCA motor finance redress scheme?

In October 2025, the FCA published Consultation Paper CP25/27, setting out detailed proposals for an industry-wide compensation scheme covering motor finance customers who were treated unfairly.2 The scheme is the FCA’s response to widespread failings in how lenders and brokers disclosed commission payments – failings that the regulator identified after reviewing thousands of case files.

The legal foundation was laid by the Supreme Court’s judgment on 1 August 2025 in Johnson v FirstRand Bank Ltd and two related appeals.3 The Court found that where a commission was high, disclosure was inadequate, and the broker’s relationship with the lender was not transparent, the credit agreement could amount to an “unfair relationship” under section 140A of the Consumer Credit Act 1974. It awarded the consumer repayment of the commission plus interest.

Following that ruling, the FCA moved quickly. The consultation proposed a structured, lender-led scheme designed to deliver compensation at scale – rather than leaving consumers to pursue individual claims through the courts or the Financial Ombudsman Service. The FCA received over 1,000 responses and is expected to publish final rules on 30 March 2026, with the scheme itself launching approximately three months later.4

Who is eligible for car finance compensation?

The scheme is deliberately broad. Under the FCA’s proposals, it covers regulated motor finance agreements – including PCP, hire purchase, and conditional sale agreements – entered into between 6 April 2007 and 1 November 2024, where a commission was paid by the lender to the broker (typically the car dealer).5

The FCA has identified three categories of arrangement that may give rise to redress:

Discretionary Commission Arrangements (DCAs) – where the broker had the ability to adjust the interest rate you were charged in order to increase their own commission. These were banned by the FCA in January 2021, but they were widespread before that date.

High commission arrangements – where the commission paid to the broker was equal to or greater than 35% of the total cost of credit and 10% of the loan amount. The FCA considers these levels to be indicative of an unfair relationship.

Exclusive or tied arrangements – where the broker had a near-exclusive relationship with a single lender, or the lender had a contractual right of first refusal. If that tie was not disclosed, the FCA treats this as a factor pointing towards unfairness.

The FCA estimates that up to 14.2 million agreements may fall within scope, of which around 44% – representing agreements where disclosure was inadequate – are likely to qualify for redress.4 There is no minimum claim value: even low-value cases are eligible.

How much compensation could you receive?

The FCA has estimated an average payout of around £700 per agreement, with total industry-wide costs projected at approximately £8.2 billion in direct redress (and up to £11 billion including implementation costs).4 However, individual amounts will vary considerably depending on the type and size of the commission, the length and value of the agreement, and the interest rate you were charged.

For cases involving discretionary commission arrangements where the commission was very high, redress may be calculated as the higher of the commission paid to the broker or an amount based on applying a retrospectively adjusted APR to the agreement. For other qualifying cases, the FCA has proposed a hybrid calculation averaging those two approaches, unless the adjusted-APR method produces a higher figure. In all cases, compensatory interest will be added at the Bank of England base rate plus 1%.4

It is important to be realistic: not every agreement will produce a large payout, and the scheme is designed to deliver fair outcomes at scale rather than windfalls. But for consumers who were charged inflated interest rates because of hidden commission arrangements, the amounts involved can be significant.

Do you need to make a claim, or is it automatic?

It depends on whether you have already complained to your lender. The FCA’s scheme sets out two separate tracks:56

If you have already complained – you will be automatically included in the scheme unless you choose to opt out. Your lender must contact you within three months of the scheme starting and tell you whether you are owed redress and how much.

If you have not yet complained – the scheme works on an opt-in basis. Your lender must contact you within six months of the scheme starting and invite you to participate. If they cannot trace you, you have up to one year from the start date to contact them directly.

Our advice is straightforward: if you think you may be affected, complain to your lender now. Doing so means you will be automatically included when the scheme goes live, and you are likely to receive any compensation sooner. You can complain directly – you do not need to use a claims management company or solicitor to do so. However, if the process feels complicated or you are unsure whether you have a valid claim, professional guidance can help ensure your case is handled properly and that nothing is missed.

When will car finance compensation be paid?

The FCA is expected to publish final rules on or around 30 March 2026.1 Based on the regulator’s most recent statements, the scheme is expected to launch approximately three months after those rules are published – meaning a start date around the end of June 2026.4

Once the scheme is live, the FCA has said that consumers who have already complained should receive a redress determination within three months of the launch. Those who opt in later will be contacted and assessed on a rolling basis. The FCA’s stated objective is for millions of consumers to receive compensation during 2026.6

Why this matters: the car finance mis-selling scandal in context

It would be easy to view this as a narrow dispute about commission disclosure. But the reality, as recent academic research has emphasised, is that the car finance scandal sits within a much longer pattern of financial mis-selling in the UK – one that stretches back through PPI, endowment mortgages, and pensions.7

In a detailed analysis published by Cambridge University Press in 2026, Dr Asta Zokaityte of the University of Kent traced the structural similarities across these episodes. In each case, financial products were distributed through intermediaries who were paid by commission. In each case, those commissions created incentives that were misaligned with consumers’ interests. And in each case, the regulatory response focused primarily on improving disclosure and providing redress after the damage was done – without fundamentally addressing the business model that produced the harm in the first place.7

The car finance market follows this pattern closely. PCP agreements – the dominant form of motor finance in the UK – are structured around low monthly payments that defer a large “balloon” payment to the end of the contract. Industry data shows that over 75% of PCP customers do not pay the balloon and instead roll into a new agreement, effectively renting rather than owning their vehicle.9 Research has found that nearly a quarter of consumers could not correctly answer basic questions about how their PCP contract works, even among university graduates.8

This matters because, for many people, a car is not a luxury – it is essential for getting to work, accessing healthcare, and managing daily life, particularly outside major cities. By 2018, over 90% of private new car purchases were financed.10 The FCA’s own Financial Lives survey found that 28% of UK adults were struggling financially as recently as early 2024,11 and StepChange, the UK’s leading debt charity, reported a 15% rise in clients with car finance debt between 2020 and 2023.12

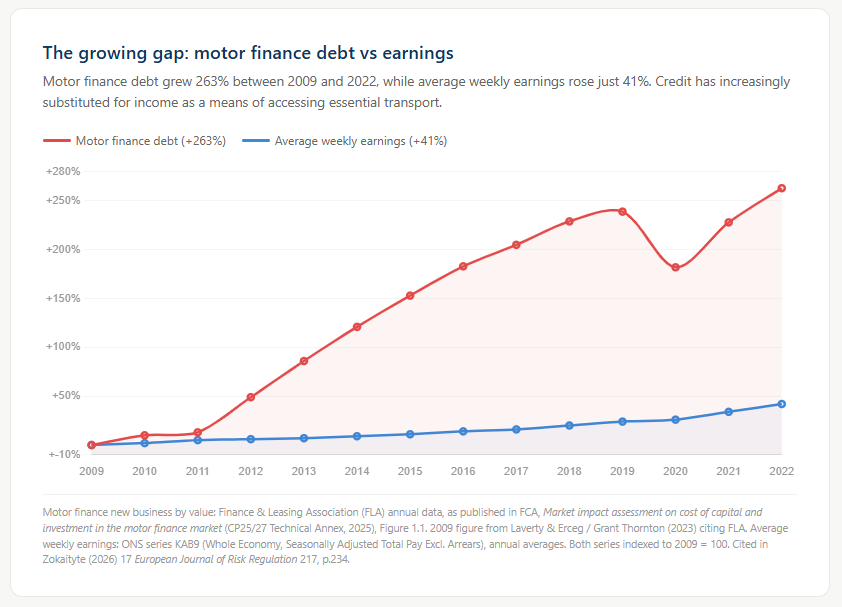

Motor finance debt in the UK grew from £11.2 billion in 2009 to £40.7 billion in 2022 – a 263% increase – while average earnings rose by just 41% over the same period.13 When credit grows that much faster than incomes, and when the products themselves are complex and commission-laden, the conditions for widespread consumer harm are firmly established.

How can Allegiant help?

We want to be upfront about this: the FCA has made clear that you can complain to your lender directly and that you do not need to use a claims management company. We agree. Many straightforward cases can and should be handled that way.

But not every case is straightforward. Some consumers had multiple finance agreements with different lenders. Some are unsure which lender they dealt with, or whether their agreement involved a DCA, a tied arrangement, or both. Some have had complaints rejected in the past and want to understand how the new scheme changes things. And some simply find the process stressful or confusing and want someone to manage it on their behalf.

That is where we come in. Allegiant is authorised and regulated by the FCA. We have been working on car finance commission claims since this area first emerged, and we have the regulatory knowledge and operational infrastructure to assess your eligibility, manage your complaint, and pursue compensation on your behalf.

If you think you may be affected by the FCA’s motor finance redress scheme, you can check your eligibility with us at no upfront cost. We will review the details of your finance agreement and let you know whether we think you have a claim worth pursuing.

Frequently asked questions

Can I claim if I had a PCP finance agreement?

Yes. PCP agreements are the most common type of motor finance and are squarely within the scope of the FCA’s proposed redress scheme. If your PCP agreement was entered into between 6 April 2007 and 1 November 2024 and commission was paid by the lender to the broker, you may be eligible.

Is the FCA redress scheme automatic?

It is automatic for consumers who have already complained to their lender. If you have not yet complained, you will need to opt in when your lender contacts you, or contact your lender directly within one year of the scheme’s launch. Complaining now means you will be included automatically.

Do I need a solicitor or claims management company?

Not necessarily. The FCA has designed the scheme so that consumers can participate without professional help. However, if your circumstances are complex or you would prefer expert support, an FCA-authorised claims management company like Allegiant can handle the process for you.

How much compensation will I get for car finance?

The FCA has estimated an average payout of approximately £700 per agreement. However, this is an average across millions of cases. Individual payouts depend on the size and type of commission, the length of your agreement, and the interest rate you were charged. Some consumers will receive more; others less.

What is the FCA motor finance scandal?

Between 2007 and 2024, many car dealers acting as credit brokers received commissions from lenders without properly disclosing them to consumers. In some cases, brokers could increase the interest rate you paid in order to boost their own commission. The Supreme Court ruled in August 2025 that this could amount to an unfair relationship, and the FCA is now implementing a compensation scheme for affected consumers.

Will I be contacted about car finance compensation?

If you have already complained, your lender should contact you within three months of the scheme starting. If you have not complained, your lender is required to contact you within six months of the launch to invite you to opt in. However, contacting your lender proactively – or lodging a complaint now – is the fastest route to receiving any compensation you are owed.

When will car finance compensation be paid?

The FCA publishes final rules on 30 March 2026, with the scheme expected to launch around three months later (end of June 2026). Consumers who have already complained should receive a redress determination within three months of launch. The FCA aims for millions to receive compensation during 2026.

What if my lender has gone into administration?

The FCA’s scheme is lender-led, so the availability of redress may be affected where a lender has entered insolvency. If your lender is in administration, it is still worth lodging a claim with the administrators, as motor finance liabilities may be dealt with as part of the insolvency process. We can advise on the position for specific lenders.

This article is provided for general information purposes and does not constitute legal or financial advice. The FCA’s final rules on the motor finance redress scheme had not been published at the time of writing (25 March 2026). Eligibility for compensation will depend on the individual circumstances of each case and the final terms of the scheme. Allegiant Finance Services Limited is authorised and regulated by the Financial Conduct Authority (FRN 836810).

References

- FCA, “Timing of the FCA’s motor finance announcement” (24 March 2026). fca.org.uk

- FCA, “CP25/27: Motor finance consumer redress scheme” (7 October 2025). fca.org.uk

- Hopcraft v Close Brothers Ltd; Johnson v FirstRand Bank Ltd; Wrench v FirstRand Bank Ltd [2025] UKSC 33 (1 August 2025).

- Grant Thornton, “Motor Finance Redress Scheme: FCA Consultation and Industry Implications” (2025). grantthornton.co.uk. Figures cited include FCA estimates from CP25/27 and subsequent updates.

- FCA, CP25/27, chapters 4–6 and draft instrument (Appendix 1); Hogan Lovells, “The road to redress: FCA’s motor finance commission consultation explained” (2025). hoganlovells.com

- FCA, “Motor finance compensation scheme to include implementation period” (March 2026). fca.org.uk

- A Zokaityte, “UK Car Finance Mis-selling: Reassessing Legal and Regulatory Challenges within Consumer Credit Markets” (2026) 17 European Journal of Risk Regulation 217–239. The analysis of recurring mis-selling patterns spans pp.221–228.

- Zokaityte (n 7), pp.229–230, citing TJ McElvaney, PD Lunn and FP McGowan, “Do Consumers Understand PCP Car Finance? An Experimental Investigation” (2018) 41 Journal of Consumer Policy 229.

- Zokaityte (n 7), p.231, citing Finance & Leasing Association and industry data indicating over 75% of PCP customers do not pay the balloon payment.

- Y Bhagat and others, “Car Ownership: Evidence Review” (National Centre for Social Research 2024); also cited in Zokaityte (n 7), p.229.

- FCA, “Financial Lives Cost of Living (Jan 2024) Recontact Survey” (2024); also cited in Zokaityte (n 7), pp.233–234.

- StepChange Debt Charity, “Helping Your Customers Drive Forward: Why Debt Advice Matters in the Automotive Finance Sector” (2023); also cited in Zokaityte (n 7), p.234.

- Zokaityte (n 7), p.234, citing C Laverty and J Erceg, “Motor Finance Bracing for Headwinds” (Grant Thornton 2023). Motor finance figures from FLA annual data; earnings from ONS Average Weekly Earnings (KAB9).